Is Skrill Safe for Casino Payments in the UK?

Is Skrill safe for casino UK payments? The cautious answer is that Skrill is a regulated e-money and payment-service brand, not a UKGC casino licence. Skrill Limited is FCA-authorised for issuing electronic money and providing payment services, but that does not tell you whether a casino is licensed, fair or suitable for you. Casino safety still depends on the gambling operator, its UKGC public-register record for Great Britain, current terms, KYC checks, financial-risk controls, GAMSTOP participation and responsible-gambling tools.

Skrill can be a useful wallet layer when the operator is legitimate and the payment route is allowed. It should not be treated as a shortcut around casino verification, credit-card restrictions, self-exclusion or bonus terms. The safe decision is to check the wallet layer and the gambling-operator layer separately.

The two-regulator boundary

The most important safety distinction is regulatory scope. Skrill’s verified role here is the wallet and payment layer. The casino operator is the business offering gambling facilities, holding player balances, setting game rules, applying bonus terms and processing withdrawals. One regulated payment brand does not make an unverified casino safe.

| Layer | Primary check | What it supports | What it does not prove |

|---|---|---|---|

| Skrill wallet | FCA e-money authorisation and Skrill account terms. | Skrill is a regulated payment-service provider for e-money/payment services. | It does not prove the casino is UKGC-licensed or that a gambling offer is safe. |

| Casino operator | UKGC public register, operator name, trading name, domain and licence status. | The gambling business can be checked against official GB licensing data. | It does not prove Skrill is available or bonus eligible for your account. |

| Your transaction | Logged-in cashier, payment terms, verification status and funding source. | The route may be available for your account, amount and purpose. | It does not guarantee instant withdrawal, bonus eligibility or no further checks. |

What Skrill regulation does mean

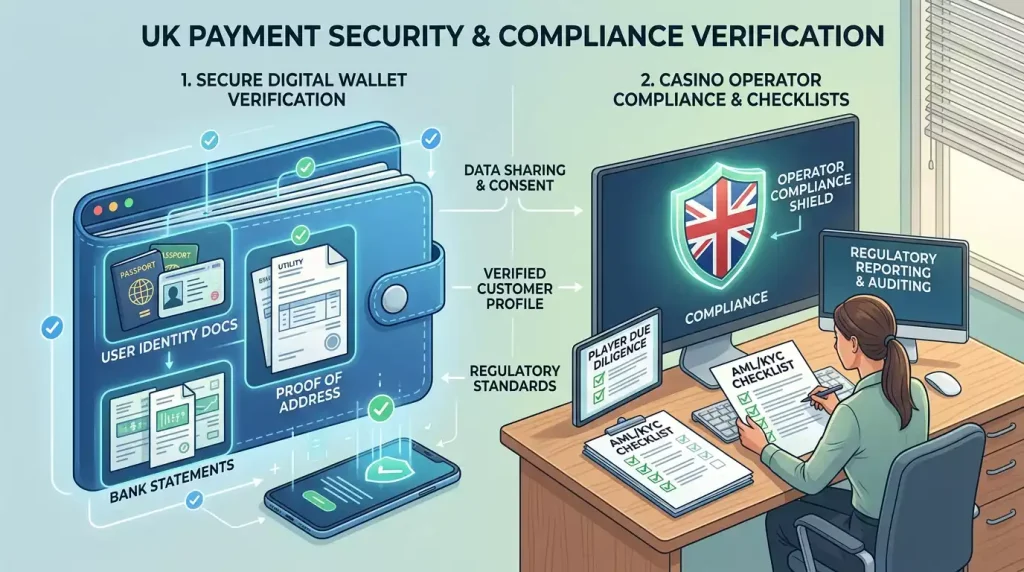

Skrill account terms describe the Skrill account as an electronic-money account that enables electronic payments. Current public terms visible during this generation state that electronic-money accounts are not bank accounts and that deposit-guarantee protection does not apply in the same way as it would for a bank deposit. This is useful context for risk. A wallet is not the same as a bank account and not the same as a casino balance.

The terms also say account upload, payment and withdrawal limits can depend on country of residence, verification status and other factors. That means a safety assessment should include your actual Skrill account status. Another person’s payment success, limit or verification outcome does not prove the same result for you.

For everyday account safety, use basic wallet hygiene: unique passwords, device security, prompt review of transaction history and immediate action if anything looks wrong. Avoid treating a casino account, a Skrill account and a bank account as interchangeable. They are separate accounts with separate controls and dispute routes.

What casino safety still requires

For Great Britain, the UKGC remote-sector guidance says businesses need a licence if they provide remote gambling facilities to consumers in Great Britain. The public register lets users search gambling businesses by business name, trading name, domain name or account number. That is the right starting point before treating a casino as licensed.

Do not stop at a badge in the footer. Check that the legal operator name, domain and trading name match the register. Look at the licence status, the activity type, any domain details and whether the casino page links to the relevant public-register information. If you cannot match the consumer-facing brand to a licensed operator, pause rather than relying on Skrill acceptance as a trust signal.

This research set did not verify a UKGC remote casino operating licence for a casino operator called Skrill. That is why this site treats “Skrill casino” as search language for payment-method guidance, not as a claim that Skrill itself operates a UK casino.

KYC and financial-risk checks are not optional extras

A common unsafe claim is that using an e-wallet makes casino play anonymous or verification-free. That is not a safe assumption. UKGC-licensed operators have obligations around age, identity, anti-money-laundering controls and customer interaction. The wallet route does not remove the casino’s need to know who is gambling and whether risk indicators require action.

Current UKGC material also refers to light-touch financial vulnerability checks at defined net-deposit thresholds, with the lower threshold described as more than £150 net deposits in a 30-day rolling period from February 2025. The important point for a Skrill user is not the threshold alone. It is that operator-side checks can still happen even when a wallet is used.

Plan for verification before it becomes urgent. Use consistent personal details, keep documents current and understand that withdrawals can pause while an operator completes checks. Skrill may also require its own verification for account limits or receiving funds. Two sets of checks can exist at the same time.

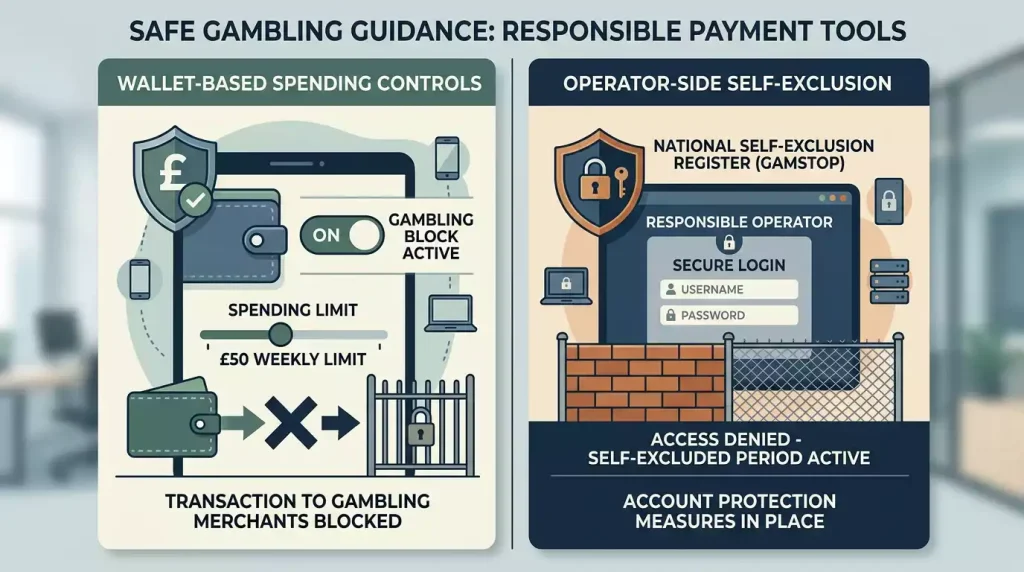

GAMSTOP and Skrill’s gambling block are different controls

GAMSTOP is the multi-operator self-exclusion scheme connected to UKGC-licensed online operators. The Gambling Commission announced that online operators must participate in GAMSTOP from March 2020, and the scheme is designed to help users exclude from participating online gambling operators through one request.

Skrill’s gambling block is a wallet-level spending control. Skrill support says that, once activated, the block declines transactions categorised under a gambling merchant category code before they go through, including payments at gambling websites using the Skrill account balance, Skrill Prepaid Mastercard payments and Skrill 1-tap payments. Skrill also states that payouts from gambling merchants and some existing recurring payments are outside the block.

Those controls can complement each other, but they are not substitutes. GAMSTOP targets operator access. A wallet gambling block targets certain payment attempts through Skrill. Someone experiencing harm should use operator self-exclusion and support tools rather than relying on a wallet feature alone.

Credit-card and e-wallet restrictions still matter

The UK credit-card gambling restriction is relevant to wallet use because e-wallets can be used as a funding layer. UKGC material says major e-wallet and e-money providers, including Skrill, gave assurances that customers cannot transfer funds to gambling operators if those funds were loaded from a credit card. Skrill support also warns that credit-card deposits for gambling may be prohibited depending on country of residence.

Do not treat Skrill as a workaround for a blocked credit-card route. If a payment depends on credit-card-funded wallet money, that is a red flag. Safer wording is simple: use only funding routes that the wallet, the casino and UK gambling-payment rules allow for gambling.

Great Britain and Northern Ireland wording caveat

Many users search “UK” as a single market, but gambling-law wording is not always identical across the United Kingdom. The Gambling Commission regulates remote gambling offered to consumers in Great Britain and the National Lottery across the UK. Its own guidance says it does not regulate the provision of remote gambling in Northern Ireland, although advertising remote gambling to Northern Ireland consumers can still involve a Gambling Commission licence.

For a practical reader, this means two things. First, GB-facing casino licence checks should be made against the UKGC register. Second, broad UK claims should be treated cautiously where Northern Ireland is involved. This page does not give legal advice and does not claim that all licensing details are identical across England, Scotland, Wales and Northern Ireland.

A practical trust checklist

- Identify the casino operator, not just the brand name or logo.

- Search the UKGC public register for the business, trading name and domain if the site serves Great Britain.

- Confirm that Skrill appears in the logged-in cashier for your account and route.

- Read payment terms for deposits, withdrawals, account limits, fees and method matching.

- Read bonus terms separately because Skrill acceptance does not prove bonus eligibility.

- Expect identity, customer-interaction and financial-risk checks from the operator where required.

- Use GAMSTOP and casino self-exclusion tools for gambling access, and consider Skrill’s gambling block as an additional payment control.

- Keep a dated record of the terms you used for your decision.

When Skrill can be a reasonable route

Skrill can make sense when you have already verified the casino operator, the cashier supports Skrill for your account, the funding source is allowed, fees and limits are acceptable, and you understand the withdrawal path. It can also help users separate gambling payments from day-to-day bank-card exposure, provided they still set their own limits and do not use the wallet as a way to blur spending.

It is weaker when the casino is not verified, the operator does not list Skrill in current terms, the bonus depends on unclear e-wallet wording, or the payment is being attempted to bypass a restriction. A wallet should improve clarity. It should not be used to make a risky casino look safer than it is.

Red flags before using Skrill at a casino

- The casino promotes “not on GAMSTOP” positioning to UK users.

- The site claims Skrill makes gambling anonymous or removes KYC.

- The footer licence details cannot be matched to a UKGC public-register record for the domain or trading name.

- The cashier accepts a deposit route but the withdrawal route is vague.

- The bonus page says Skrill is eligible but the official terms are silent or contradictory.

- The site encourages a credit-card-funded wallet workaround.

- Support refuses to confirm payment, licence or bonus terms in writing.

What Skrill cannot verify for you

Skrill can help show whether a wallet payment route exists, but it cannot verify the gambling operator for you. It cannot prove that the domain you are using belongs to the licensed operator, that the casino’s bonus terms accept e-wallet deposits, that a payout will pass the operator’s review, or that a customer-interaction check will not be triggered. Those are operator-side and regulatory-side questions.

This is why a Skrill logo should be treated as one signal, not a safety certificate. The logo may indicate that a cashier route is advertised or available, but the safest review still checks the legal entity, the domain, the current payment terms, responsible-gambling tools and the withdrawal path. If the operator details are unclear, Skrill acceptance does not repair the missing trust evidence.

A low-risk test decision framework

When you are still unsure, think in terms of exposure. Do not use a bonus as the reason to rush. Start by deciding whether the operator passes the licence and domain checks without considering the offer. Then decide whether Skrill is the right payment method without considering the bonus. Only after those two answers are positive should you consider whether the promotion terms make Skrill eligible.

This sequence reduces a common mistake: using a large headline offer to justify a weak operator check or an uncertain payment route. A safe payment decision should stand on its own. A bonus can improve the value of a deposit only when the underlying site, wallet route and terms are already acceptable.

What “safe” should mean for a Skrill casino payment

In this context, safe does not mean risk-free and it does not mean approved by Skrill. A safer Skrill casino payment is one where the operator is identifiable, the GB licence position can be checked, the cashier clearly supports Skrill, the wallet balance comes from an eligible source, and the user understands the withdrawal and verification route before playing. Each layer should be checked before money moves, because a mistake at one layer can make the whole transaction unsuitable.

It also means knowing when not to proceed. If the site hides the operator name, if the bonus terms are unclear, if the payment page implies that Skrill bypasses checks, or if support cannot explain the withdrawal route, the safer action is to pause. A wallet can make payment management cleaner, but it cannot repair weak casino evidence or unclear gambling terms.

Bottom line

Skrill can be safe enough as a payment layer only when the surrounding checks are safe enough. Its FCA e-money authorisation is relevant to the wallet. It is not a casino licence, not a guarantee of casino legitimacy, not a proof of bonus eligibility and not a way around KYC, GAMSTOP or credit-card restrictions. For UK readers, the most useful safety rule is to verify the casino first, verify the Skrill route second and treat every bonus, limit and withdrawal claim as operator-specific.

This material was created by the Skrill UK Guide team.

Play only with verified operators using the reviews on the homepage.

Manage your account restrictions at any time by learning how the Skrill gambling block works.

Related posts

Skrill KYC and Casino Verification UK

Skrill Gambling Block and GAMSTOP: What Each Does in the UK